The Impact of Blockchain Technology on Ecommerce

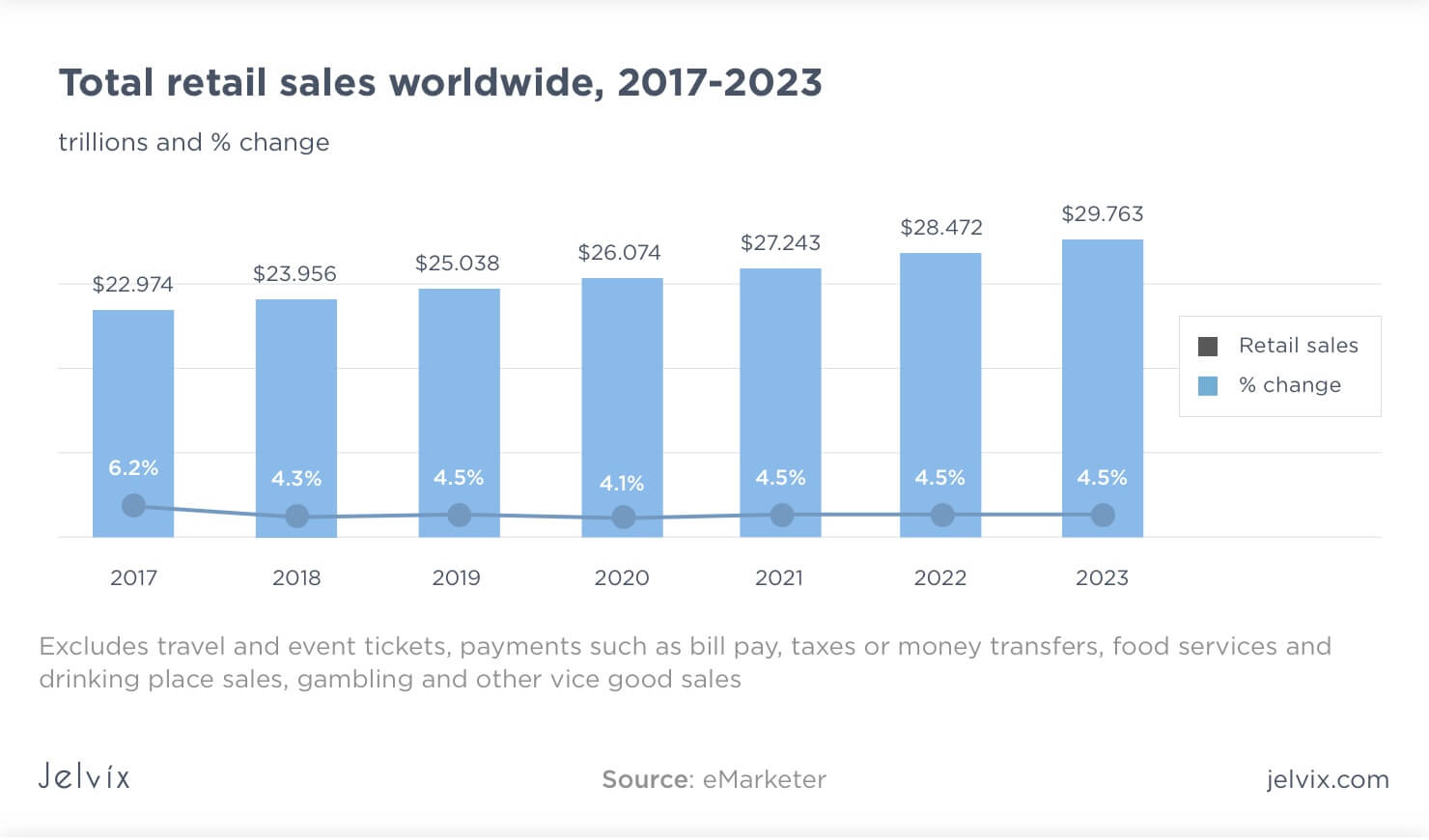

Over the last decade, the global eCommerce industry has experienced tremendous growth. According to the latest estimations from eMarketer, the online retail market will reach more than $25 trillion by the end of this year, which translates into a 4.5 percent growth compared to 2018. While these figures certainly sound impressive, this year’s performance is actually worse compared to previous years.

Take a look at the image below. There, you’ll see that the growth rate has declined from the five preceding years, where the industry was growing by at least 5.7 percent.

The decline in the global eCommerce industry is an outcome of a myriad of factors. The growing economic uncertainty, worsening business conditions in many market leaders, ineffective business practices, cybercrime, and the need for faster and more efficient logistics are among them.

In other words, despite the growing number of online shoppers, the industry is affected by a number of inefficiencies and drawbacks that may prevent it from sustaining the ever-growing demand. A large share of these drawbacks and inefficiencies relate to outdated practices.

For example, in the global logistics industry, issues like transaction fees, the rising cybercrime, intermediaries, and a slow contract execution are a major burden that costs billions of dollars now. As a result, they’re slowing down the global eCommerce trade.

To cut a long story short, the eCommerce industry needs a disruption.

By “disruption,” I mean positive change that will sweep away inefficient and outdated practices.

Blockchain: the disruption of the fourth industrial revolution?

Fortunately, we can confidently claim that technology now has an answer to address the challenges faced by the global eCommerce industry: blockchain. The ability of this technology to track, authenticate, improve security and execution of contracts, guarantee the transaction of data and information, and deliver other things make it a perfect tool to apply across the entire value chain.

Recently, a number of well-known eCommerce companies, including Amazon, have been actively exploring the use cases of blockchain in the industry. We’ve already seen some projects being done; for example, shortly after announcing a managed blockchain service in late 2018, Amazon had opened this service for everyone in May this year.

The service is called Amazon Managed Blockchain (no surprises here), and it “makes it possible to build applications where multiple parties can execute transactions without the need for a trusted, central authority.”

With retail giants like Amazon working on their own blockchain-powered systems and tools, the eCommerce industry stands to benefit big. In fact, this recent report from IHS suggests that the business value is projected to reach $164 billion by 2030.

“Using blockchain within the retail and e-commerce sector can lead to a direct relationship opportunity with the customer, providing companies with greater understanding of their needs and behavior,” Business Wire quoted Don Tait, senior blockchain analyst, as saying. “Blockchain and smart contracts can also provide the tools and framework to create a new generation of marketplaces.”

Without a doubt, now is the high time for eCommerce companies to explore the benefits of blockchain and take advantage of them to avoid being outcompeted by others. But what are the benefits that blockchain has for them? How is this technology already changing the industry?

4 ways blockchain is transforming eCommerce industry

Experts say that the use of blockchain in the next few years will be limited to creating decentralized marketplaces, handling online payments, improving supply chains, and helping companies with contract execution with smart contracts.

However, new use cases are quickly emerging, so let’s take a look at proven solutions that blockchain has to offer in eCommerce.

1. Improving international logistics

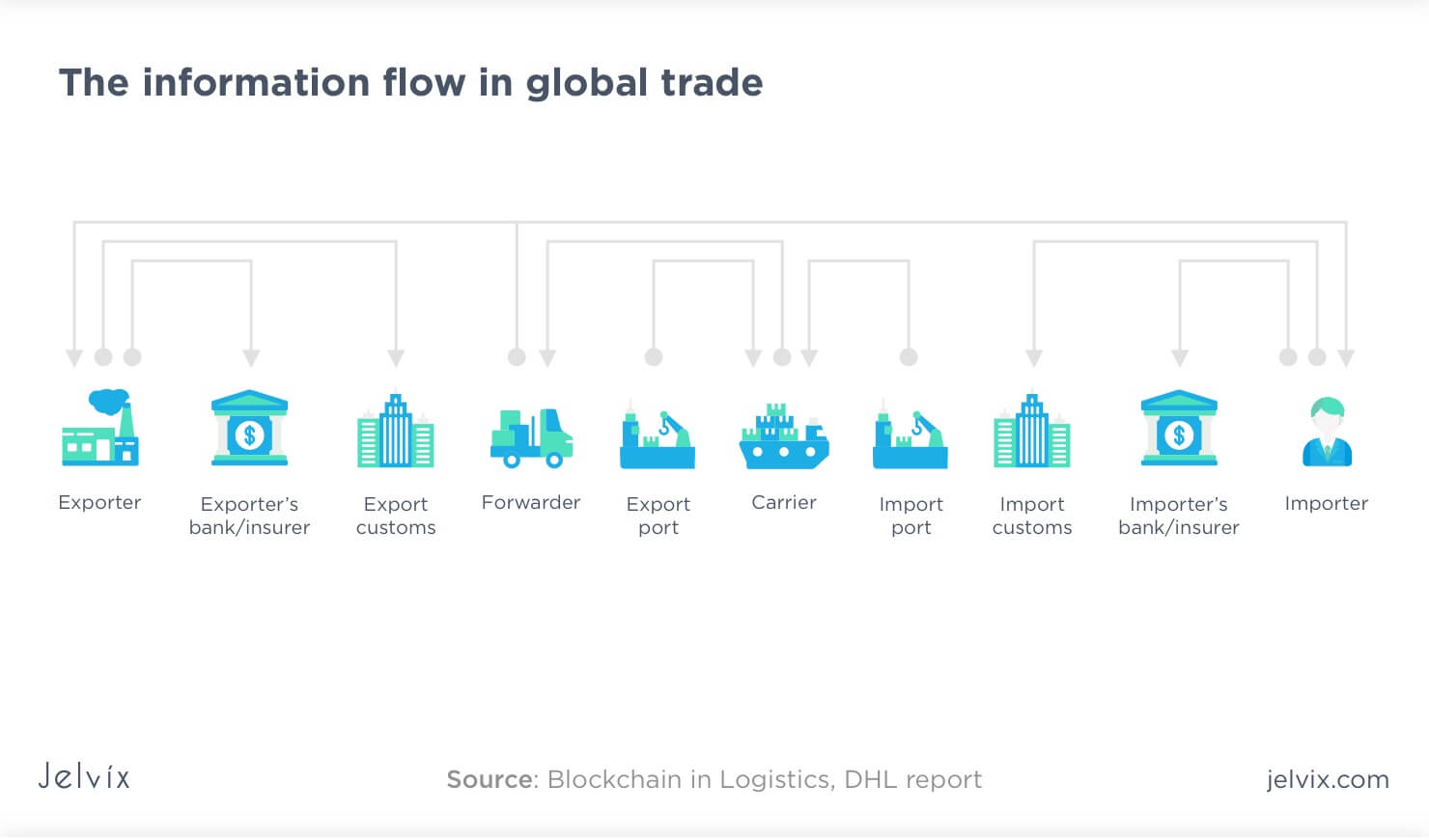

Removing the need for intermediaries is a dream of every logistics professional. The flow of information and data in international logistics and trade is highly complex and is plagued with intermediaries and inefficiencies. On top of that, it’s extremely documentation heavy, which makes a quick flow of goods almost impossible in most cases.

According to this blockchain report from DHL, this is how complex the information flow is in global trade.

DHL claims that there’s a significant amount of trapped value in logistics, which is a result of the industry being very competitive and fragmented. To support this point, the authors cite the fact that the US alone has more than 500,000 trucking companies. Eventually, with so many stakeholders involved in the supply chain, the adoption of more efficient and transparent practices is painfully slow.

Blockchain is increasingly seen by logistics companies as a tool for reducing the following issues:

- A lack of transparency and traceability in eCommerce supply chain

- A lack of automation of commercial processes which leads to disputes and other process inefficiencies.

While the second one is more related to financial transactions, it still has a profound effect on logistics (we’re going to talk about it in more detail in the next section).

So, let’s focus on how blockchain can improve tracking & tracing and create more transparency by cutting middlemen in the global supply chain.

For eCommerce companies, getting rid of middlemen standing between them and their suppliers would be a huge deal.

The main benefit would be the reduction or elimination of intermediaries in financial transactions that occur in eCommerce supply chains.

For example, if the supplier’s bank utilizes blockchain to enable financial operations with the eCommerce company, there may be no need to employ a trusted intermediary. This, in turn, eliminates the need for corresponding banks as well (think about fewer fees and faster overall logistics).

Blockchain is also applicable for tracking all activities and actions in the eCommerce supply chain, helping to answer the following questions:

- Who is performing an activity/action?

- When the activity/action was performed?

- What is the location of each activity/action?

- What is the progress of delivering goods?

- Which products are included in a shipment?

This can dramatically increase traceability in supply chains, and many companies have already conducted tests to define how effective blockchain really is here. One prominent example is WalMart, and they’re exploring the application of the technology to enhance the transparency and traceability of the supply chain.

According to reports, Walmart has been actively involved in tracking supplies with blockchain technology. For example, they’ve already tracked Indian-sourced shrimp supply chains to selected locations in the US and now have expanded the tracing functionality to more than 25 products from 5 different suppliers. For that, they’re using the IBM’s Hyperledger food traceability system, which was initially built to trace pork supplies from China.

Here are the foods that the American retail giant is currently tracking with the system to ensure authenticity and reduce the risks of poor quality products injected into the supply chain, according to IBM’s report on Walmart.

The blockchain-based system has been working well for Walmart so far. Together with IBM, the retail company now is able to track the origin of the above-mentioned products within 2.2 seconds (they needed at least 7 days to do so before the Hyperledger).

This is not the only way blockchain ensures the integrity of the supply chain. A number of blockchain companies are now pushing for decentralized marketplaces designed to enable peer-to-peer commerce. For example, OpenBazaar is such a marketplace that simplifies commerce between retailers and suppliers by minimizing the number of middlemen.

Unlike centralized sellers like eBay and Amazon, OpenBazaar places users completely in control, as they can interact with each other directly, and use cryptocurrency to pay. Since there’s no middleman like banks, there are no limits, credit card fees, or need to create a seller account.

Here’s an illustration showing how blockchain-enabled peer to peer platforms like OpenBazaar work.

Further evolution of blockchain will surely lead to more simplified eCommerce transactions, which is something that both customers and sellers will appreciate.

2. Improving cross-border financial transactions

Delayed payments and subsequent issues are something that every eCommerce seller is familiar with, as the industry still mostly relies on inefficient practices. Despite having numerous options such as PayPal, Venmo, and a pretty sophisticated global system of trade finance, eCommerce industry players are still facing a lot of problems:

- Substantial fees, often as high as 10 percent

- A very limited range of options that offer cross-border payments

- High exchange rates.

As a result, conducting cross-border eCommerce transactions is nothing but easy.

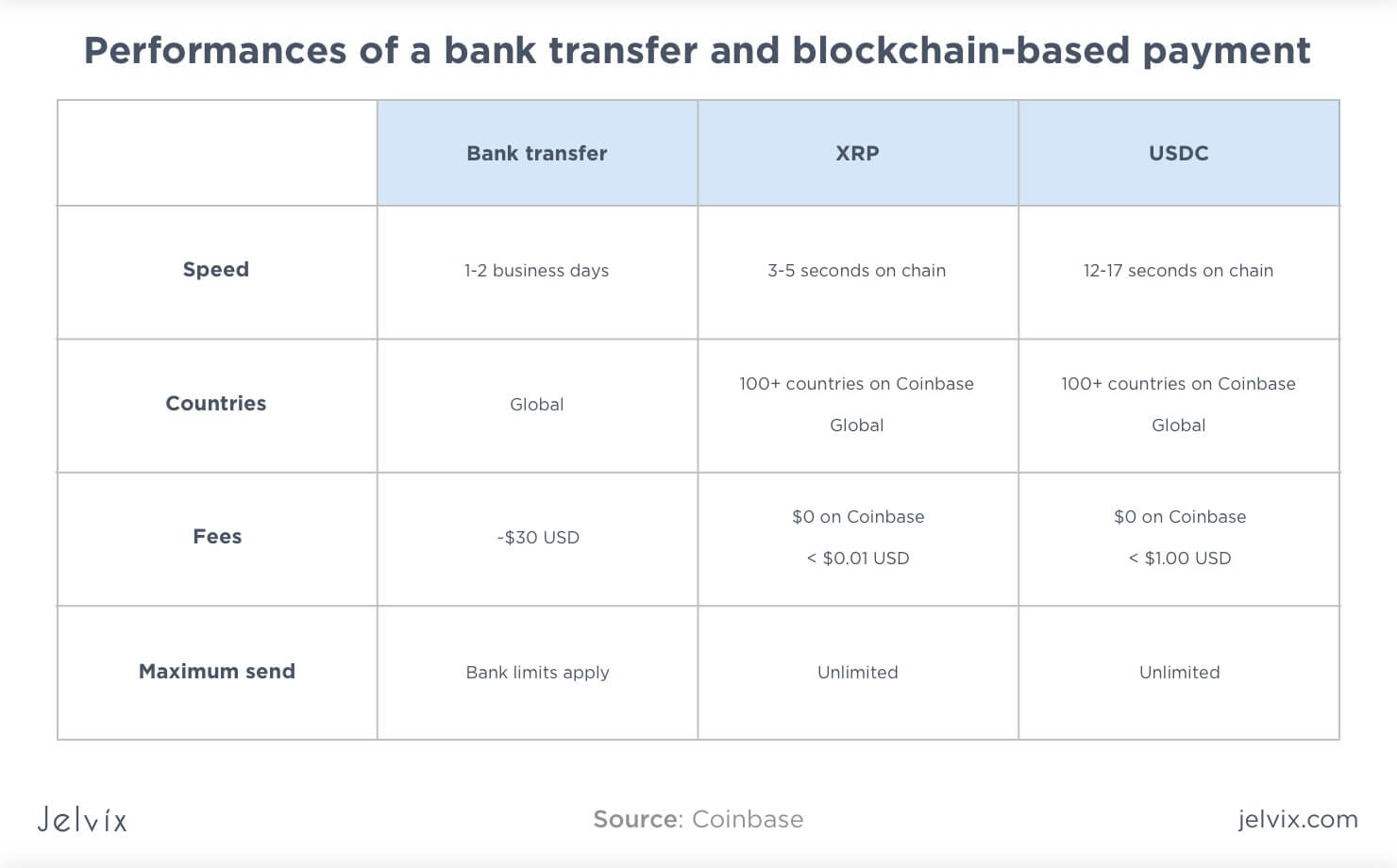

On the other hand, cryptocurrencies are the way to substantially reduce or even eliminate bank fees and exchange rates while paying internationally, thus saving money for eCommerce businesses. Paying with a cryptocurrency also ensures faster validation or credit payments because of the lack of banks involved in the transaction.

Companies like Coinbase are already making this happen. For example, this company charges only a flat 1 percent fee for converting a cryptocurrency into local currency, thus removing the need for banks and even governments. By using similar services, eCommerce companies can pay suppliers by sending money across borders almost instantly using XRP or USDC. Here’s a comparison of performances of a traditional bank transfer and blockchain-based international payment.

3. Improving eCommerce contract execution

Another major application of blockchain technology in global eCommerce finance is smart contracts. Simply defined, a smart contract is a program controlling the transfer of digital assets and the immediate enforcement of conditions. Their main use cases in eCommerce include:

- Automation of commercial processes in logistics

- Improving reliability and security of online marketplaces

- Automatic enablement of customer loyalty programs.

First, smart contracts can help to automate commercial processes in eCommerce logistics by allowing them to execute contractual conditions automatically. For example, if a party says a supplier doesn’t fulfill a condition, the funds would be held. So the contract won’t be fulfilled.

In fact, the above-mentioned DHL report on blockchain says that 10 percent of all freight invoices contain inaccurate data, which results in a lot of disputes. By using smart contracts, the number of disputes between eCommerce sellers and their suppliers can be reduced dramatically.

Second, smart contracts can improve the security and reliability of online marketplaces. For example, if a customer checks out on an eCommerce website, the money paid for the product or service would be held in the smart contract. The seller, in turn, would have to proceed to approve the act of the purchase and redirect the contract to the delivery company.

Third, eCommerce sellers can program smart contracts to enable certain customer-related features. For example, it could be a solution to automatically enable customer loyalty programs as a smart contract store the information about purchase history and issues rewards and bonuses once a customer reaches a certain threshold.

Deloitte has explored the application of blockchain for customer loyalty programs in the banking industry and concluded that it was an effective way to engage more people to use loyalty points. According to this report, the initiation of a loyalty transaction in a smart contract – exchange, issuance, redemption, etc. – the blockchain-enabled protocol generates a special token where all rewards accumulate.

By giving customers access to rewards through the loyalty application, which is essentially a digital wallet, companies make it easy for people to redeem their points.

As a result, a smart loyalty program can incentivize customer behavior and increase loyalty, which is something that becomes increasingly important for eCommerce companies. For example, 82 percent of online businesses agree that customer retention is cheaper than acquisition; besides, 75 percent of online shoppers say they favor companies that offer rewards.

4. Prevention of eCommerce fraud

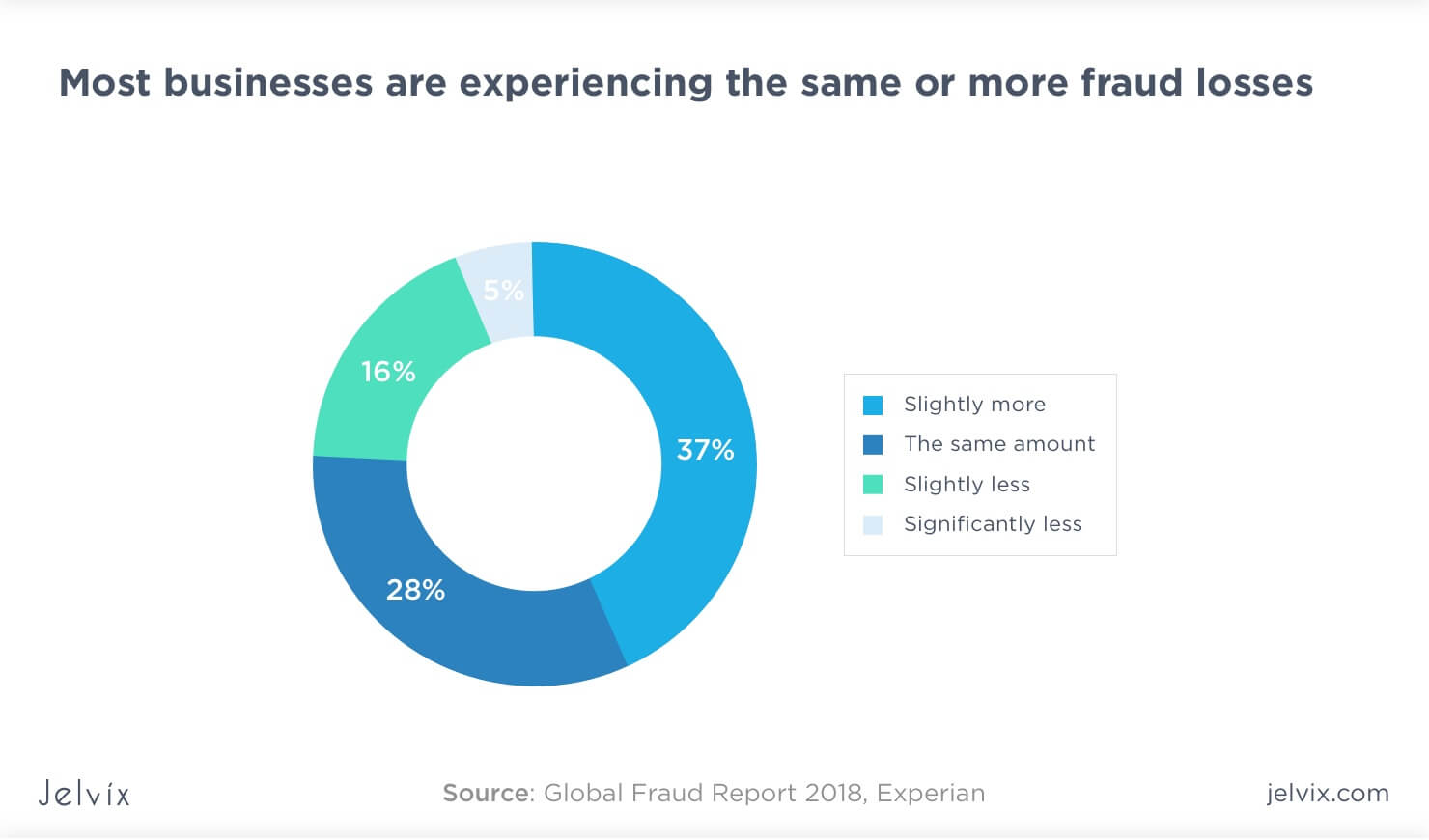

eCommerce businesses use a wide variety of fraud detection and prevention methods, but the issue continues to grow. According to the Global Fraud Report 2018 from Experian, 65 percent of businesses are detecting “the same or more fraudulent activity.”

This, combined with the fact that 75 percent of online businesses want advanced security systems, makes a pretty convincing case for the application of blockchain.

Let’s consider the example of chargeback fraud. Simply explained, it happens when a customer requests a chargeback from the issuing bank after receiving the product, thus forcing the credit card transaction to be reversed. Many people actually confuse chargebacks with refunds, but the two work a bit differently.

The bank returns the funds that a customer paid for the product from a business’s account until the decision is made if the whole request was valid. If it is, the customer gets their money back, so the main purpose of chargebacks – protecting people from poor quality products – is achieved.

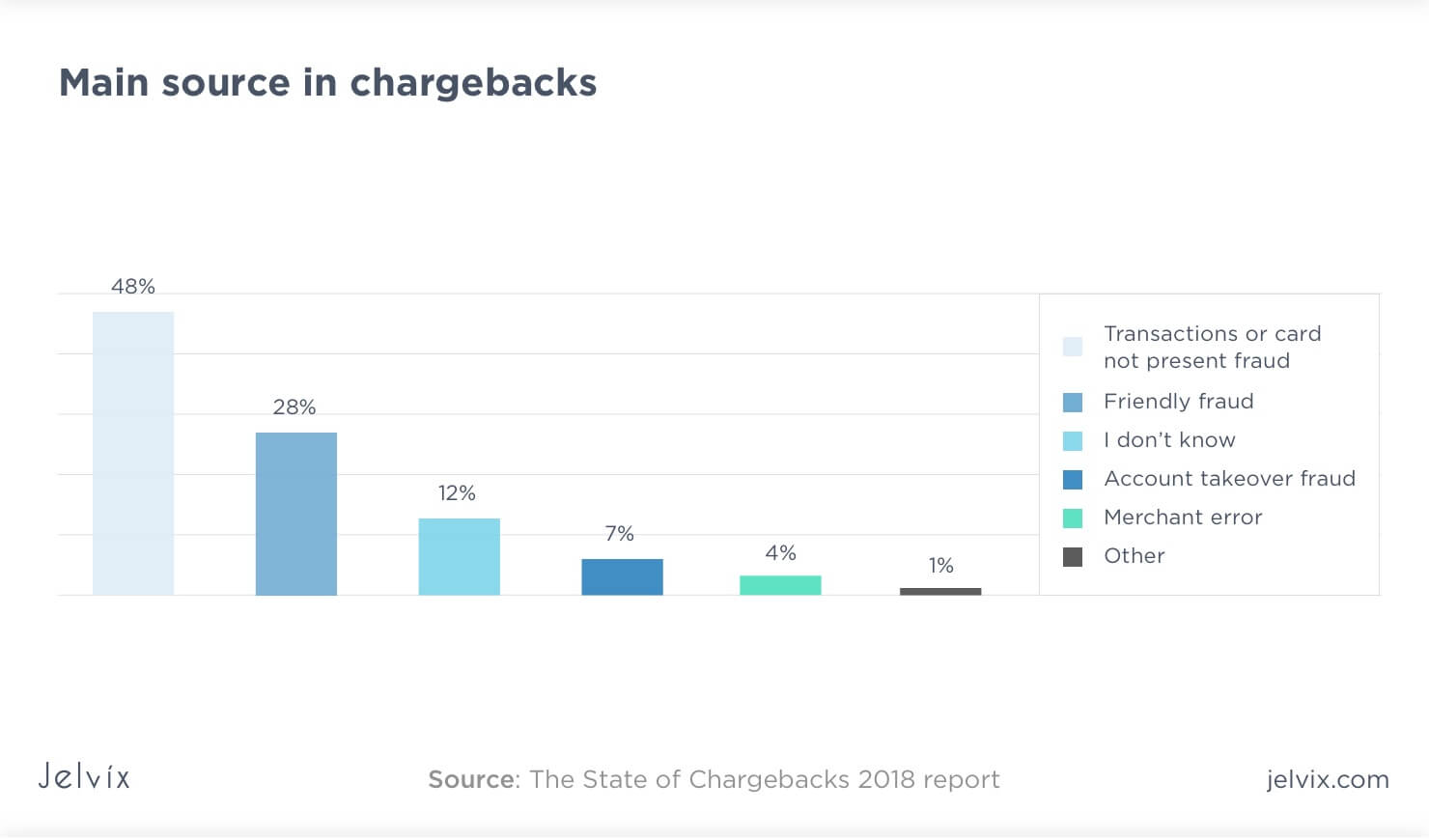

However, in many cases, chargebacks are made with fraudulent intent. A fraudster will request the chargeback in an attempt to get the money back while retaining the product rendered. According to The State of Chargebacks 2018 report, 48 percent of chargebacks they receive are made with fraudulent intent.

So how can blockchain help eCommerce businesses to reduce this issue?

Well, chargeback fraud is almost impossible in case if an eCommerce seller uses blockchain-enabled payment systems and smart contracts (it’s possible only if a real mistake was made). As mentioned above, smart contracts ensure that the money paid for a product is released to the seller only when pre-specified conditions are met. The conditions are embodied in the code of the contract.

This means that once the seller’s account has been credited with the money of the customer, there’s no way the latter can reverse it (the fact that this transaction was completed automatically means that the customer is satisfied). The nature of smart contracts allows them to cover a range of typical agreements between eCommerce sellers and customers, including product shipment fees and product purchases.

On top of that, the payments made on a blockchain-enabled system are conducted instantly, so hackers simply have no time to interfere with them.

So, with no opportunity to reverse eCommerce payments, fraudsters won’t have as many chances to penetrate the schemes of online sellers, all thanks to blockchain. That’s why transfers based on this technology are increasingly considered the most secure type of online financial transaction.

Final thoughts

The global eCommerce value is growing, but it needs a major disruption to sustain the growth rate. The chances are that blockchain will be that much-needed positive disruption that will finally start sweeping away those outdated and inefficient practices. With many eCommerce giants exploring the technology as well as young firms developing innovative solutions based on blockchain, it’s safe to assume that we’re going to see blockchain in the news many times in 2020 and beyond.

eCommerce is not the only industry that’s being changed by blockchain, though. If you’re interested in knowing why this technology has been so successful in bringing changes to law & government, healthcare, energy, food, tourism, and real estate industries, check out Why Blockchain Transforms so Many Industries guide.

Kristin Savage is interested in writing and planning to publish her own book in the nearest future. Also, she has been a reviewer at Pick Writers for a few years and is known for her thorough approach to accurately assess newcomer translation services. You can find her on Facebook.

Comentarios

Publicar un comentario